This blog post is an excerpt from the Advanced Energy Now 2023 Market Report, prepared for Advanced Energy United by Guidehouse Insights. This post is the fifth in a series of excerpts from the report.

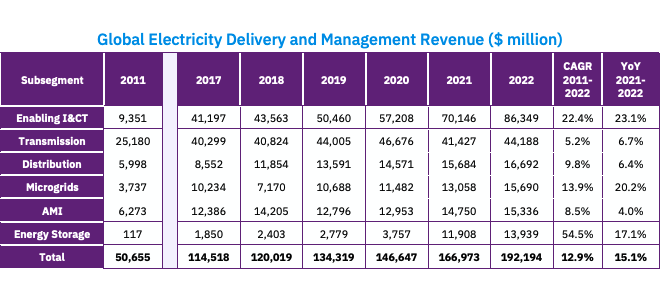

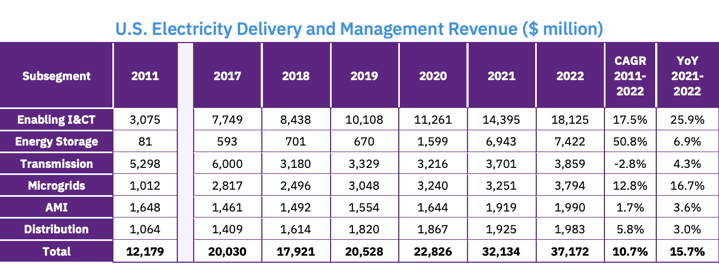

Worldwide, Advanced Electricity Delivery and Management (ED&M) products and services, which includes a subset of the overall ED&M market, achieved an 11% compound annual growth rate (CAGR) for the period 2017 to 2022; in the U.S., the CAGR was 13% over that same period.

The year 2022 was the biggest for the segment since we started tracking it in 2011, recording 15% annual growth globally and 16% in the U.S. While global growth was slightly slower in 2021, at 14%, ED&M grew significantly in the U.S. (+41%) due to the proliferation of large-scale energy storage. The impact of energy storage technologies on total market growth has been quite significant over the past two years. For example, when excluding the Energy Storage subsegment, ED&M annual market growth in 2021 falls from 14% to 9% globally, and from 41% to 19% in the U.S.

Even so, taking out this high-growth subsegment shows that there was still solid growth in other areas, such as advanced metering infrastructure (AMI) and enabling information & communications technology (IC&T), both of which have experienced strong recoveries post-COVID-19. With the passage of the Infrastructure Investment and Jobs Act (IIJA) in 2021, and the Inflation Reduction Act (IRA) in 2022, which include billions of dollars for clean energy generation, transmission, and distribution upgrades, ED&M products are expected to continue to receive significant investment in the coming decade. (In fact, just last month, the U.S. Department of Energy’s (DOE) Grid Deployment Office awarded $3.5 billion for 58 grid-improving projects as part of the Grid Resilience and Innovation Partnerships (GRIP) Program.)

Total revenue in the global ED&M market is traditionally led by sizeable investment in large-scale advanced transmission infrastructure, defined as HVDC systems, submarine transmission systems, and smart transmission system upgrades, as well as the IC&T that supports grid management. Broadly, the market for advanced transmission technologies is relatively mature, with moderate growth (2% CAGR 2017-22) expected to continue, and occasional sizable year-to-year swings from particularly large infrastructure projects. That said, the need to integrate offshore wind and large-scale solar should continue to support advanced transmission investments.

In comparison, Enabling IC&T has grown more consistently over the past five years, with a CAGR of 16%. The fastest growing subsegment globally, while still moderately sized, has been Energy Storage, with a CAGR of 50% from 2017 to 2022 and 17% last year, reaching $13.9 billion in annual revenue.

In the U.S., ED&M revenue has grown at a strong rate over the past five years (CAGR of 15.7%) but with a pronounced shift among subsegments. Advanced transmission, which comprised over 40% of U.S. ED&M revenue in 2011, has dropped from $6.0 billion to just under $3.9 billion in annual revenue since 2017.

Unlike advanced transmission, Enabling IC&T has grown steadily in the U.S., at a CAGR of 19% from 2017 to 2022 and 26% last year, reaching $18.1 billion in annual spending in 2022. Meanwhile, investment in Energy Storage has taken off, especially in 2021 (which saw 334% growth over 2020), increasing to $7.4 billion in annual spending in 2022, achieving an overall 51% CAGR since 2011.

Transmission Constraints and Interconnection Challenges Put Net Zero Emissions Goals at Risk

Globally, the year-over-year growth in spending on advanced transmission technologies – like HVDC lines, submarine power cables, and smart transmission system upgrades – declined in late 2020 and early 2021, resulting in an 11% decrease in 2021 relative to 2020, likely due to further economic contraction from the COVID-19 pandemic. Post-pandemic recovery has seen growth in spending rebound by 7% in 2022.

The same is not true of the U.S., where the rate of growth in spending on advanced transmission systems increased by 15% in 2021 relative to 2020, and another 4% in 2022 relative to 2021. Because transmission planning in the U.S. can take years, many advanced transmission investments landing in 2021 and 2022 were the result of transmission expansions planned well before the pandemic. This may explain the relative strength of U.S. investments in advanced transmission over the last two years. Consequently, a drop in U.S. spending on advanced transmission sometime in late 2023 or early 2024 would not be surprising.

That said, with the passage of the IIJA and IRA, the U.S. will be investing billions of dollars towards replacing fossil fuels with low-carbon and zero-emissions alternatives and building out the transmission and distribution system required to get clean power to where it is needed. The IIJA appropriated nearly $5 billion specifically for transmission expansion, a relatively small investment considering that Guidehouse Insights data indicates that nearly $3.9 billion in new transmission projects are being added each year. The IRA provides additional funding for transmission, including: $2 billion to the U.S. Department of Energy (DOE) to provide low- or no-interest financing for transmission projects deemed in the national interest; roughly $1 billion to the DOE for grants to assist states in siting transmission lines; $100 million to the DOE to conduct analysis and planning for offshore and interregional transmission planning; and $5 billion to help the DOE retool and repower existing transmission projects. Until new transmission infrastructure comes online, however, clean energy projects will continue to face significant challenges in getting approved to connect to the U.S. transmission network.

Although spending on transmission in the U.S. has steadily increased in recent years, it is not nearly enough. Delivering clean energy in the U.S. to where it is needed to meet net zero emissions targets may require building the equivalent of the current U.S. transmission and distribution infrastructure over the next 25 years, a cumulative investment of several trillion dollars. Interconnection of clean generation in the U.S. also remains a tedious and painstaking process requiring advanced system modeling to determine the exact system upgrades that may be necessary to ensure that project can connect to the grid without threatening safety and reliability. FERC, the DOE, and the U.S. Congress are aware of the interconnection problem and are working to address it, but reforms will take time to come into effect. Should various proposals to quicken the interconnection process be implemented, investments in new transmission—including the advanced transmission technologies covered in this report—would likely follow pace.